2019 | Year of Anaemic Growth for SA

SA ENTERS TECHNICAL RECESSION IN FINAL QUARTER OF 2019

South Africa’s Gross Domestic Product (GDP) declined by 1.4% (y/y) in the fourth quarter of 2019, following a revised 0.8% contraction in the previous quarter (2019:Q3). This marked the second consecutive quarter of negative growth, pushing the SA economy into a technical recession. The local economy registered a meagre 0.2% improvement for 2019, compared to the 0.8% and 1.4% annual growth registered for 2017 and 2018, respectively.

SA REGISTERS ECONOMIC GROWTH BELOW MARKET CONSENSUS

QUARTERLY PERFORMANCE UNPACKED

Unlike the rebound in economic activity recorded in the second quarter of 2019, the lacklustre performance for the fourth quarter of 2019 saw the domestic economy enter its second technical recession in two years and marked the third contraction in economic activity in a one year.

BROAD-BASED ECONOMIC PERFORMANCE A DISSAPPOINTMENT

The sluggish outcome was attributed to a contraction in the three-broad sectors; particularly in the secondary sector.

Performance in the secondary sector deteriorated by -2.6% owing to subdue activity across all sectors. The largest contraction of -5.9% was observed in construction activity, which was chiefly due to a protracted downturn in residential buildings, non-residential buildings and construction work during the period. Consequently, this was sector’s sixth (6th) consecutive contraction. Notwithstanding, the FNB/BER Building Confidence Index improved in the fourth quarter of 2019 from 22 to 25 index points with the only concern being around the cost of building materials among respondents.

WILD CARD SECTORS REGISTER DIVERGENT RESULTS

Utilities regressed by -4.0% due to the re-emergence of load shedding in October 2019 which adversely affected the income generating capabilities of many enterprises. Similarly, manufacturing activity decreased by -1.8%. The weak performance in manufacturing was attributed to low automotive and wood and paper industry production volumes. This was corroborated by lower average hours worked per factory worker in the SARB leading indicator for December 2019. Analysts were of the view that the impediments in key intermediate goods manufacturing economies could have acted as a linchpin for the rejuvenation of the dwindling manufacturing and mining sectors as established global value chains that depend on inputs from China came under growing strain on the back of trade talks between China and the US. Other hindrances could be evidenced by the uptick in Producer Price Inflation (PPI) since November 2019 which was highly inflated by the PPI for electricity and water.

On the other hand, mining activity improved by 1.8% during the quarter with the increase credited to stellar performance in the Platinum Group Metals (PGMs) — this was likely due to increased demand for alternative suppliers in global value chains.

CLIMATE CHANGE CONTINUES TO PLAGUE AGRICULTURE

Despite the expansion in mining activity, the primary sector recorded a 0.4% decline in production for the fourth quarter of 2019. This was appropriated to a 7.6% contraction — the largest decrease observed for the period and the fourth consecutive weakening — in agricultural activity due to a drop in yields of field crops and horticulture products. The depressed performance of the sector is mirrored in the protracted downturn in the AgBiz/IDC Agribusiness Confidence Index (ACI) following a devastating plunge in the first half of 2018 and consequent rebound of the sector (of 13.7%) in the third quarter of 2018. The ACI registered at 44 index-points for the last quarter of 2019.

IMPROVEMENTS IN FINANCE SECTOR UNABLE TO SOFTEN SUPPRESSED DOMESTIC DEMAND BLOW

The finance sector recorded the highest growth for the period, expanding by 2.7%. The growth was credited to increases in financial intermediation and auxiliary services which were possibly spurred by the rate cut in September 2019 and quantitative easing across several global central banks. However, the growth in the sector was eclipsed by sluggish figures for the transport (-7.2%), trade (-3.8%), households (-0.7%) and community services (0.4%) sectors, which resulted in the tertiary sector contracting by 1.0% over the quarter.

WHOLESALE TRADE VALUE CHAIN IMPLICATIONS

Given the seasonal effects in trade activity during the fourth quarter of each year, mainly owing to “Black Friday” and festive spending sprees, the dreary trade performance was unexpected. The decline in activity was chiefly due to lower wholesale and motor trade together with accommodation services, indicative of generally suppressed domestic demand. This is further supported by the drop-in sale of passenger vehicles, lower automotive export sales and the wholesale trade measure under the FNB/BER Business Confidence Index (BCI). According to FNB/BER, the BCI wholesale confidence plunged from 42 index-points in the second quarter of 2019 to 28 index-points for the last quarter of 2019. This was largely due to anaemic demand for non-consumer goods. Likewise, this softer wholesale trade confidence reading could partially explain the sluggish figures in the manufacturing as non-consumer goods are generally used as input production for the sector.

ANNUAL PERFORMANCE UNPACKED

The South African economy expanded moderately by 0.2% (y/y) in 2019. This was below the market consensus of between 0.3% and 0.4% growth.

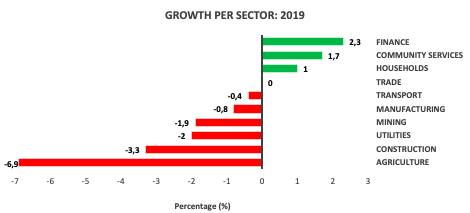

GDP 2019

The increase was stifled by contractions in six (6) out of the ten (10) sectors namely; agriculture (-6.7%), construction (-3.3%), utilities (-2.0%), mining (-1.9%), manufacturing (-0.8%) and transport (-0.4%). Conversely, increased output was registered for finance (2.3%), community services (1.7%) and household (1.0%) activity; while trade activity remained flat at 0.0%.

The flat growth is trade activity is corroborated by declines in expenditure sub-components such as export for goods and services (-2.5%), gross fixed capital formation (-0.9%) and import for goods and services (-0.5%). While, the contraction in agricultural activity is synonymous with registered decrease in production in all four quarter for 2019.

ECONOMIC GROWTH OUTLOOK

Economic growth for the country remains on the downside in the near-to-medium term. Key deterrents to growth will stem from the uncertain energy supply, climate change and the exogenous effects of the Corona Virus outbreak on supply chains. However, the implementation of key pronouncements both the SONA and budget such as the tapering of the public wage bills, personal tax relief and the lag effects of rate cuts in 2019 could soften the hard landing expected for the economy for 2020.

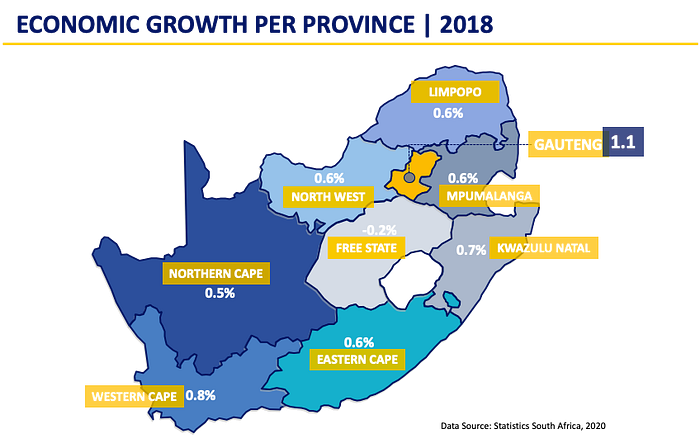

PROVINCIAL ANALYSIS | GAUTENG LEADS THE PACK

Similarly, in the latest national GDP publication, Statistics South Africa released the provincial growth figures for the 2018.

Akin to moderate growth for the country of 0.8% in 2018, the provincial growth figures mimicked the depressed national output. The largest growth was recorded in Gauteng at 1.1%, followed by Western Cape (0.8%) and Kwa-Zulu Natal (0.7%). Whilst a contraction of -0.2% was registered in the Free State likely due to the drought during the period.

The uptick growth in Gauteng in 2018 in comparison to 2017 -where Gauteng registered the second lowest growth rate- is likely attributed to the consistent performance of the finance sector during the period and implications of headquarter bias. Further in a high concentration of activity in eight (8) of the ten (10) sectors, apart from mining and agriculture. However, concerns on the production capacity of the manufacturing sector are impeded by structural bottlenecks, cost push inflation and intermitted electricity supply.

Given the steady performance of the finance sector and the dwindling in the production of other sectors due to depressed global and domestic demand in 2019, Gauteng growth is likely to continue on the ledge.